The global demand for natural gas was 3.9 trillion cubic metres (tcm) in 2018, a 4.9% increase from 2017. OECD (Organization for Economic Development) countries experienced a 4.5% increase in demand for natural gas, while non-OECD countries experienced a 5.3% increase. Global gas trade surpassed the 1.2 tcm threshold in 2018. This growth can be attributed to the increase in global Liquefied Natural Gas (LNG) trade which grew by 7.3% in 2018. The prices of LNG also continued the trend of convergence, while import prices for the USA, EU, Japan and Korea all increased.

The exact composition of natural gas mostly depends on the source. Natural gas is made up of 60 – 90% methane, about 20% ethane, propane, butane and trace amounts of other gases, such as Nitrogen. When composition is almost pure methane, it is known as ‘dry’ natural gas. The presence of heavier hydrocarbons makes it ‘wet’. The heavier hydrocarbons removed in order to increase the methane presence in natural gas are referred to as Natural Gas Liquids (NGLs).

Natural Gas Transportation

Most of the world’s natural gas is delivered through pipelines, with a large network of pipelines delivering natural gas to processing facilities, as well as end consumers. Natural gas is compressed to enable pipeline transportation. The pipeline networks can be categorised into three:

In the situation natural gas cannot be delivered on land, it can be liquefied and transported by ships. Natural gas is condensed to a liquid by cooling it to -260 °F (-162°c). Liquefied Natural Gas (LNG) occupies 600 times less volume than natural gas at atmospheric temperature; this and the liquid state enables easy storage and its transport by road, rail or ship (using methane carriers). LNG is shipped from terminals and the shipment is received at terminals, where it is regasified. There are several types of LNG terminals, differing based on technology used:

The Floating Storage and Regasification Unit (FSRU)

The FSRU can be classified either as a (special kind of) ship or an offshore installation. Most FSRUs are classified as ships to enable flexibility in operating them either as a FSRU or an LNG tanker. FSRUs are to be located close to the coast, inside a port or a protected area. FSRUs can be equipped in two ways:

The FSRU business began in 2001, with the first FSRU built for the Gulf Gateway Project. By 2017, 26 FSRUs were in operation, with 23 operating as terminals and 3 as LNG terminals. The International Gas Union stated that FSRUs had a total regasification capacity of 84 MTPA (million tonnes per annum) based on estimates. The number of FSRUs have grown rapidly due to their relatively low capital cost, commercial flexibility, faster schedule and reusable asset feature. Land based terminals on the other hand are regarded as sunk cost.

A 2017 report stated that the cost of a new FSRU was 60% of an onshore terminal and could be delivered at half the time. New projects cost $240 - $300 million and could be constructed in 2-3 years, while FSRUs based on LNG tanker conversions cost $105 - $130 million and take 18 months to be converted (due to long delivery times of equipment, rather than the shipyard conversion itself). An example of a fast tracked project was the second Egypt FSRU which was completed in 5 months.

Comparison Between On-shore Terminals and FSRUs

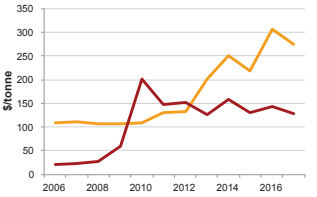

The cost of an onshore regasification has been on the rise since 2012, while that of FSRUs has remained relatively steady. The average unit cost of onshore regasification capacity that came online in 2017 was $274/tonne, while that of FSRUs was $129/tonne. It should be noted that the operating costs of FSRUs are higher than that of onshore terminals due to vessel charters associated with the project.

Figure 1. Regasification Costs Based on Project Start Dates

Source: International Gas Union. World Gas LNG Report, 2018.

Additionally, some FSRUs are used for power generation, by independent electricity companies which plan to serve developing countries. Many FSRU companies now generate power on the FSRU or on an adjacent barge, to provide a one-stop shop solution.

FSRUs consist of the following essential components:

In 2018, the Lagos State government was in talks with Golar LNG Limited to acquire an FSRU, to provide energy security in case the gas pipeline from Delta is shut down for any reason.

It is possible that with time, the FSRUs will evolve to provide other important services and it is paramount that such innovation is used to its greatest advantage.

The number of FSRUs in operation is expected to increase as demand also increases. FSRUs might be used by some nations to act as gas terminals while onshore terminals are constructed. Other nations would use FSRUs to generate electricity. Generally, adoption of FSRUs is expected to increase over the years such that the International Gas Union (IGU) expects 50 FSRUs in operation by 2025.

The Nigerian LPG Market is the next success story of the Global LPG industry, if you need a partner with a global perspective and local expertise in the Nigerian and African space, kindly book for a free session with our team of experts to help you http://www.kiakiagas.com/book-session or write us an email at advisory@kiakiagas.com or Whatsapp: +2348085269328