Angola’s economy is heavily dependent on hydrocarbon production; Angola’s dependence on oil revenue has made its economy vulnerable to crude oil price volatility. The country ranks second among oil producing countries in sub-Saharan Africa. It is also an OPEC member with output at approximately 1.37 million barrels per day (bpd) and a production of level of about 17,904.5 million cubic feet of natural gas. There have been a significant drop in production due to drop in Oil price and limited investment in both new or older exploration and production for most part of 2014 to 2018. The negative impact of limited investments has led Angola to the current daily lifting of 1.37 million barrels of oil per day (bpd), far below capacity.

This recent development in the oil and gas industry is inspiring the introduction of reforms, involving new investment that are expected to increase production in the medium to long-term. The government has also been implementing a macroeconomic stabilization program to reduce its fiscal deficit, improve exchange rate flexibility, and strengthen governance to attract greater private sector investment.

Angola’s Oil industry is influenced by Upstream– exploration and production of offshore crude oil and natural gas. Though the country is a leading oil producer in the region, the bulk of the oil production have typically come from off-shore sources. These sources contain light sweet crude oil with minimal Sulphur content usually preferred for processing light refined petroleum products. The continental shelf off the coast of Angolan has been partitioned into 50 blocks. However, more blocks is envisaged to be created in subsequent rounds of auctions.

Exploration and production

The Lower Congo and Kwanza Basins host much of the offshore proven reserves of oil and gas. Most survey activity in Angola is conducted offshore at depths of more than 1,200 meters (3,937 feet).According to a research done by Business Monitor International (BMI), recent exploration prospects are primarily focused on the Lower Congo and Kwanza Basins, with the bulk of the drilling targeting deepwater and presalt formations. Most of the drilling is carried out by industry supermajors and Sonangol. Nearly all the Oil productions in Angola comes from offshore fields off the coast of Cabinda and deepwater fields in the Lower Congo Basin. The country’s oil production grew by an average of 15% from 2002 to 2008 annually since production started in several deepwater fields discovered in the 1990s. Ever since, IOCs led by Total, Chevron, ExxonMobil, and BP have started production at additional deepwater fields and are developing new ones.

Survey activities in Angola’s onshore was said to be restricted during the past decades because of the civil war (1975–2002).Over the past few years,onshore exploration has recommenced but at a much slower pace than offshore activities.

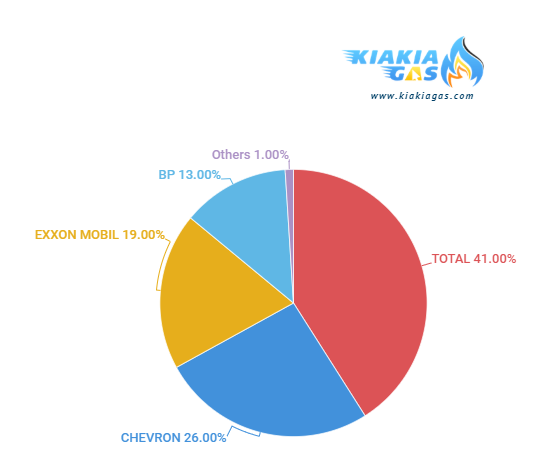

Major Oil exploration and production players active in Angola include Total, with 41 percent market share (800 bpd), Chevron with 26 percent market share (510 bpd), Exxon Mobil with 19 percent market share (375 bpd), and BP with 13 percent market share (252 bpd).Other international players include ENI and Equinor. Sonangol also operates through its subsidiary Sonangol E&P. they are different projects and partnership contracts ongoing inorder to enhance it’s LPG growth.

Angola Natural Gas Market players

Ultra-deep-water projects are being acquired by Total in Block 32 (USD 16 billion Kaombo project expected to peak at 230,000 bpd), and BP's "Pluton, Saturn, Venus and Mars" (PSVM) project in Block 31 (USD14 billion). U.S. company MODEC supplied an accommodation vessel to support the tie up operations on BP’s PSVM project.

Onshore activities are very restricted as SOMOIL, a privately-owned company, was planning to produce around 5,000 bpd in Soyo, in northern Angola, but operations have been put on hold. U.S is currently active in the Angolan upstream market. Some of the U.S contractors include: Halliburton, Baker Hughes a GE Company, FMC Technologies, Oceaneering, etc. Other countries that are in one way or the other providing services and investing in Angola include the UK, Norway, France, Italy, Korea and China. Korean exports to Angola consists mainly in offshore platforms and vessels. While Chinese exports focus on low cost equipment and commodity inputs such as pipes.

Midstream and downstream activities:

Angola’s new liquefied natural gas (LNG) plant situated in soyo, was built to commercialize much of its natural gas and reduce the flaring of gas. There are plans to also develop some previously discovered non–associated natural gas fields. Angola LNG is a consortium that includes Sonangol (22.8%), Chevron (36.4%), Total (13.6%), BP (13.6%), and Eni (13.6%). According to Angola LNG, the $10 billion LNG project was the largest single investment in Angola’s history. The forecast of the plant was to be able to produce to produce 5.2 million tons per year (250 billion cubic feet per year) of LNG, as well as natural gas plant liquids. The plant suspended operations owing to technical difficulties in 2015 and 2016, but then restarted in early 2017. Offshore shipments go to Brazil, China, South Korea and France. The U.S. was a target market, but it has not materialized due to increased U.S. domestic production.

Currently, the downstream sector – refinery of crude oil and distribution of products derived from crude oil – remains well below domestic demand.

With offshore oil exploration continuing at a Steady pace, Angola will need to address its capacity for processing the large volumes of associated gas its oil operations will continue to produce. Improving LNG capabilities, developing the domestic market for commercial natural gas, and applying enhanced oil recovery techniques will be important components to Angola’s natural gas strategy moving forward.

Energy consumption

Low prices of fuel in Angola has played a major role in the rise of the demand for oil. A report by the World Bank on Angola’s Fuels subsidy reform reveals that the price of oil in Angola are among the lowest in the world. Between September 2014 to January 2016, the government implemented a series of fuel price increases, removing all fuel subsidies except a 40% and 10% subsidy for LPG and kerosene, respectively.

Despite being the third-largest economy in sub–Saharan Africa with regards of official GDP approximately, 30% of Angolans live below the poverty line of less than $1.90 per day, based on 2011 levels of purchasing power parity. Most people use traditional solid biomass and waste consisting typically of woods, manure, charcoal, and other crops remains to find cooking needs and off-grind heating

Renewable energy sources

Hydropower is the dominant source of power generation for the country, primarily from hydroelectric dams on the Kwanza (Cuanza), Catumbela, and Cunene Rivers. Some analysis suggests that the country's potential hydroelectric generating capacity is at least 10 times the current installed capacity. Hydropower will continue to be the dominant source for the near future, given the government’s focus on developing hydropower capabilities as a source for electricity. Mostly in rural areas where the electrification rate was only 16%, compared to 71% in urban areas, in 2016.

Conclusion:

Solar and wind power are potential substitutions to power generation. Angola’s 2025 Vision outlines the country’s long–term energy strategy and highlights some of the studies conducted to identify regions with the greatest potential

for solar and wind capacity. However, the country has yet to develop significant solar and wind power generation projects, and it is unclear whether it intends to pursue such projects in the near future.

References: World Small Hydropower Development Report 2016,

Chevron Press Release – Chevron Starts Production From Angola’s First Deepwater Oil Field

World Bank Group Open Data database,

Angola Energy 2025: Power Sector Long–term Vision, Generation,

BP 2014 Statistical Review of World Energy.